With cattle prices declining, one big question cattle producers are asking themselves is this: When and where is the bottom?

In tackling this question, one useful comparison is last year.

As producers will no doubt remember, it was in late September/early October 2016 that prices were crashing. A multi-month bear market just kept falling and falling. We know now the bottom finally occurred in October 2016.

After rallying from that low into the spring, prices turned back down and here we are a year after the great crash low, looking at some US prices back down near that same low.

Let’s compare:

- The last week of September year ago, cash US steers were averaging around US$104/cwt. They got slightly lower than that in October. Today, prices are similar at around $105.

- In late Sept. 2016 the nearby Oct 2016 live cattle future was trading under US$90. Today it’s quite a bit higher – at $108.

- In late Sept. 2016 the Feb 2017 future was predicting only a slight recovery, it was around $101. Today’s Feb future – the Feb 2018 – is showing more optimism than back then. It is at $117.

Observation from this: Cash cattle prices are almost as bad as a year ago. Futures are well above year-ago levels.

Let’s compare feeders:

- Late Sept 2016 saw the feeder cash index at $134 in late Sept and it slammed under $120 in October. Today, it stands at $149.73.

- Last year the nearby feeder futures were hanging around $125 before seeing trades under $120 in October. Today, the nearby Sept and Oct 2017 futures are in the $151-152 area.

- A year ago the March 2017 feeder future was at $116. Today’s March 2018 contract is much higher at $146.30.

Observation from this: Cash feeder prices are almost as bad as a year ago, while futures are stronger.

What’s the supply picture compared to a year ago? How is demand holding up?

We could compare all kinds of supply and demand factors to a year ago, ranging from carcass weights, cattle on feed weights and numbers, cow kill…contracted supplies, retail prices, exports and imports… but let’s focus for the time being on one basic fundamental: total production.

Stats for total beef and meat production are from the USDA. They’re not perfect; the predictions for the fourth quarter could change. Still, they form a basic framework of total supply and even if the details are off, at least the general direction looks right.

US beef production 3rd quarter (July-Aug Sept)

Last year: 6.47 billion lbs

This year: 6.83 billion lbs, up 5.5%

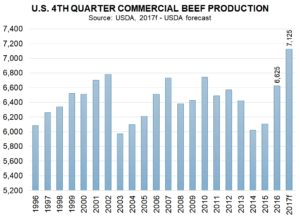

US beef production 4th quarter (Oct-Nov-Dec)

Last year 6.62 billion lbs

This year: 7.16 billion lbs, up 8.1%.

Pork and chicken output is on the rise too. Total red and white meat this quarter is predicted at 26.28 billion lbs, up 4.9% from 25.03 billion last year.

All meat production in Q1 2018 is expected to exceed that of Q1 2017, although by only 1.4%.

Observation: That is a heck of a lot of beef and total meat for the domestic and export markets to digest. It might take lower prices for consumers and importers to swallow that much. Looking only at supply, one could argue that some livestock and meat market prices will have to fall below the levels of the fall of 2016.

That said, the demand side is encouraging. Retail prices are little changed from a year ago – cases higher – even as more meat comes to town. When more is consumed and the price is steady, that means better demand. Maybe that means prices won’t have to go much (if any) lower in the fourth quarter, despite sharply rising supplies versus a year ago.

How about the charts? What are they telling us?

Sometimes chart patterns can tell us more than fundamental factors.

Right now, the futures charts do look a lot different than last year. Cattle and feeder cattle have been rallying the past few weeks. A year ago, they were rumbling downhill under the increasing momentum of their own weight.

This year, however, we don’t see that same bearish momentum. This could mean the market is more stable and less vulnerable to falling much farther.

Last year, futures markets were so out of control to the downside they bounced strongly heading into the Jan-Feb-March period. Maybe this year they won’t go overboard to the downside as much and might rally less in winter and spring.

Of note, feeder cattle cash and futures prices are not nearly as heavily pressured as a year ago. The feeder market seems to be building in ideas of a strong recovery for cash cattle markets in 2018.

Bottom line:

Cash cattle and live cattle futures could be coming into some important lows like they were last year. However, they have larger total supplies to cope with, which could tone down the fall to spring upswing.

If the feeder cattle you buy are based on the index on which futures are based and on futures prices, take note: Feeders aren’t the same low-priced buying opportunity they were a year ago.

By John DePutter & Dave Milne, DePutter Publishing Ltd.

Explore our cattle feed here.

Brought to you in partnership by: