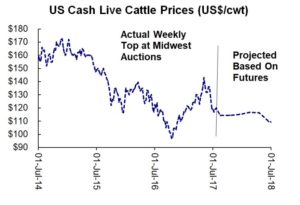

If you’ve been keeping up with these blog posts you know that we believe that the main trend for cash cattle prices is down from the high made in the spring. We’ve also suggested that although the details of the current downtrend are hard to call there’s a chance the market declines all the way to the low made in 2016 before bottoming out.

Mind you, there are a lot of moving parts in the cattle business. Drought. Trade issues. Currency shifts. Export demand. All these things play a role in determining the price level at which supply and demand start to become more balanced – and when.

We’ll update you on the demand side of the market in a future edition. Today we want to talk about the supply side.

USDA counts more cows & calves, but fewer replacement heifers

The USDA released a semi-annual inventory report on July 22. There was no comparison to last year (because that report was a victim of Washington politics). Still, the main message of this year’s report is clear: Lots of expansion has taken place the past two years.

Below are some highlights:

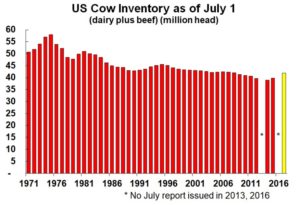

- The total inventory of US cattle and calves was 102.6 million on July 1. That was up 4% compared to July 1, 2015.

- The total cow inventory of 41.9 million head and beef cow count of 32.5 million are both up 5% and 7%, respectively compared to two years ago.

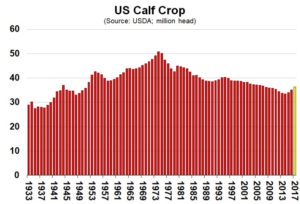

- At 36.3 million, the projected calf crop for 2017 would be up 3% compared to last year and up 6% from 2015.

The expansion shown in the inventory report isn’t a shock. After all, in 2014 and 2015 the market called for more beef by putting fat profits in front of ranchers. They responded by retaining more breeding stock, producing more calves and – in time – more beef. They got help from the weather too, with improved pasture conditions on the southern Plains following several years of severe drought.

Expansion set to slow

Looking ahead, we think the pace of expansion will moderate. In 2016 and 2017, prices and profitability have been more volatile – and at times less appealing – than during the peak years of the cattle cycle.

Don’t take our word for it though. Data in the inventory report confirms it. In particular, the number of beef replacement heifers jumps out at us. At 4.70 million on July 1, they were down 2% from July 1, 2015. This is an indication that cattlemen are starting to have some second thoughts about continuing to ramp up their herds. It will be interesting to see if this downsizing is confirmed by the next semi-annual cattle count, due in early 2018.

In addition, ongoing drought on the northern Plains and parts of the western Midwest could be causing some cattle to get moved from pastures to feedlots sooner than would normally be the case. This idea is supported by data in a regular US monthly cattle report, also released July 25. Cattle on feed on July 1 came in at 10.8 million. That was up a hefty 4% from a year earlier. Placements during June were pegged at 1.77 million, up a substantial 16% from last year. Large increases were seen in cattle states such as South Dakota and Oklahoma, parts of which are parched.

Summing up the USDA reports: Expansion of US beef production continues. There are lots of cattle in feedlots and more on the way. So, there will be lots of market ready cattle in late 2017 and early 2018. (And potentially somewhat fewer later, in 2018.)

Four quick hits to wrap up:

- Current downtrend for cash prices could continue, generally speaking. Prices are not necessarily going to truly plummet from current lower levels but with lots of beef coming down the pike, there’s certainly downside risk. The market needs to do its job of encouraging more consumption, which won’t be easy with supplies of cheaper pork and poultry also on the rise. The most likely way to stimulate more beef consumption? Lower prices.

- Live cattle futures are pricing in some of the potential weakness ahead by the cash fed steers, but maybe not all of it. As this is written the August, October and December futures are trading in the ballpark of US$114.50 to 115.50. That’s down $8-12 from where these contracts were trading in early June. It’s also about $5 under recent cash prices. However, the market remains well above the high $90s, which is where it bottomed in October, 2016.

- Proceed with caution. With some warning lights flashing, it’s not time for cattlemen to be taking on added risk. With the ongoing discounts in the futures markets, there are still not clear short-hedging opportunities for producers to prepare for whatever weakness may come in the cattle markets.

- Canadians need to heed the signals coming from the US. Although we have seen only a small amount of expansion in Western Canada in recent years, the Canadian market is smaller than the US. This means that the American marketplace plays a huge role in determining Canadian price trends. Based on what’s currently going on south of the border, some caution is warranted by Canucks as well.

By Ranulf Glanville & John DePutter, DePutter Publishing Ltd.

Brought to you in partnership by: